Deloitte’s annual Leeds Crane Survey reveals a tale of two markets across the city’s leeds commercial property sector — record-breaking residential development but new office construction remains slow.

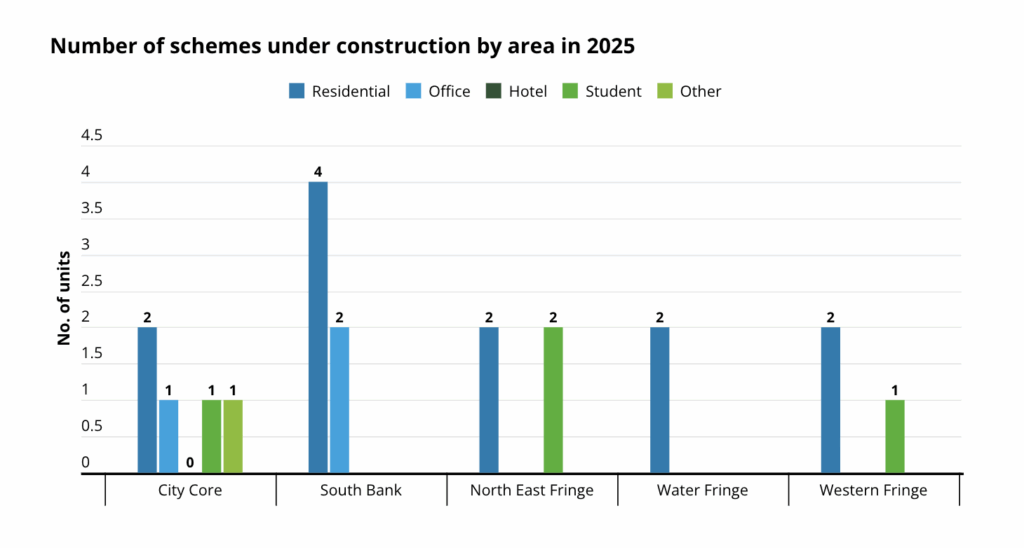

The 2026 survey shows 20 major schemes currently under construction across Leeds, delivering more than 5,900 new homes — the highest figure since records began. However, only 25,200 square feet of new office space broke ground in 2025, representing a 49 per cent drop on the previous year and signalling a dramatic shift in developer confidence.

Never Miss a Leeds Business Event

Get our monthly events guide straight to your inbox — every networking meetup, conference, and showcase happening in Leeds.

Free, no spam. Unsubscribe anytime. Privacy policy

Despite broader construction activity slowing to just eight new project starts in 2025 — the lowest since 2013 — the residential and student accommodation sectors have surged ahead. Construction began on 2,064 new homes across three schemes, up 12 per cent on 2024, while student bedspace starts jumped 84 per cent to 896 units.

The South Bank continues to dominate the city’s construction landscape, accounting for 30 per cent of all active schemes. Meanwhile, 1,914 student bedspaces reached completion in 2025, the third-highest annual total on record, underscoring continued demand for city centre living.

Leeds Commercial Property Market Shows Sectoral Divergence

The findings reflect a broader recalibration in leeds commercial property development as investors navigate persistent economic headwinds. Rising construction costs, supply chain constraints, and fluctuating interest rates have dampened speculative office development, yet residential schemes continue to attract capital.

According to the Deloitte report, Leeds is forecast to deliver annual GVA growth of 1.7 per cent between 2025 and 2028 — outpacing both the UK average (1.6 per cent) and Yorkshire and the Humber (1.5 per cent). This economic resilience, combined with easing interest rates and increased government support for regional development, is fuelling optimism among housebuilders.

Significantly, 36 per cent of developers surveyed indicated they are more likely to break ground on new projects in 2026 compared to 2025, suggesting the pipeline may soon accelerate again.

The city’s ongoing transport improvements — including the Sustainable Travel Gateway at Leeds Station and the TransPennine Route Upgrade — are also bolstering long-term investor confidence, particularly in emerging neighbourhoods along the Northeast Fringe.